WITH lockdown restrictions gradually easing in the UK and more Brits returning to work, the furlough scheme is going to be wound down.

The government ‘s coronavirus job retention scheme has allowed those unable to work due to coronavirus to claim 80 per cent of their normal wage up to £2,500 a month – but when will it come to an end?

What is the government furlough scheme?

Simply put, if your employer has been forced to close temporarily due to coronavirus, it can claim 80 per cent of your wages, which it will then pay to employees.

Claims are, however, capped at £2,500 a month for each employee, so if you usually earn a lot more than that you’ll see a bigger drop in wages.

Your company can top up the remaining money you’d usually be paid, but most businesses are taking a serious hit and have chosen not to.

Bosses can also claim employer national insurance contributions and minimum automatic enrolment pension contributions on top for wages up to £2,500 a month.

The scheme was first launched on March 20 although it was backdated until March 1.

More than 9million workers have been furloughed, although new applicants were prevented from joining the scheme from June 10.

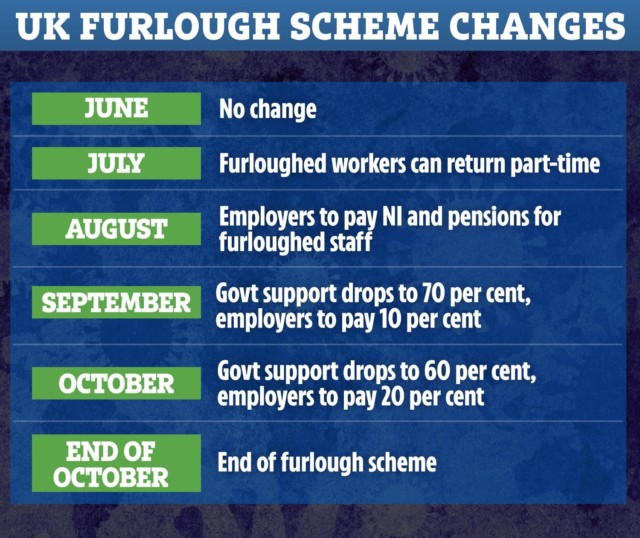

How is the furlough scheme changing?

The government announced a shake-up to the furlough scheme in June that will see a number of changes come into force from July 1 onwards.

From July 1, bosses can bring furloughed employees back to work for any amount of time and shift pattern, and still claim furlough payments for the time they are not working.

Until now, workers haven’t been allowed to work for their own company while on furlough, and they’ve also had to have been furloughed for at least three weeks at a time before working for their firm again.

From August, employers will have to contribute to wages, initially by paying national insurance and pension contributions.

From September, employers will have to pay those contributions plus 10 per cent of salaries.

Then from October they will have to pay those contributions plus 20 per cent of salaries.

{kind=link}