BANKS are bringing in 40 per cent interest on overdrafts – double the rate on the average credit card.

The changes, agreed by industry regulator the Financial Conduct Authority (FCA), were meant to happen in April but were delayed by the coronavirus pandemic.

Now they are hitting just as furlough schemes come to an end and unemployment is spiralling.

The changes are causing concern and confusion, with millions worried they will be stung with extra fees.

How it affects you depends on how you use your overdraft and my table, right, gives an idea of whether you will pay more . . . or less.

But financial experts say most people will suffer.

Sarah Coles, personal finance analyst at Hargreaves Lansdown, says: “The FCA has given the go-ahead for unfair overdraft hikes that are a bitter blow for borrowers, who face a bleaker future.

“The FCA said there was competition in the market so people could shop around for a better deal.

‘Dip in and pay price’

“Unfortunately, we know this isn’t how people use overdrafts.

“Our research shows that one in ten people faced with an unexpected expense dip into their overdraft to cover the cost.

“They don’t research the cost and switch bank accounts first, they dip in and pay the price.”

Here is a guide to what is going on — and what you can do about it.

WHY ARE BANKS DOING THIS?

The FCA ordered banks to replace their daily and monthly overdraft fees with a simple interest rate so customers could compare borrowing costs more easily.

But they were also told they cannot charge more for an unauthorised overdraft than an authorised one.

So most have upped their authorised overdraft rates to get round this. As a result, pretty much all banks started charging all overdraft users 40 per cent.

Lloyds and Halifax even began charging 49.9 per cent. For some, this has meant a major outlay.

When coronavirus hit the UK, the FCA delayed the measures, but now they are being introduced across the board, while some banks started last month.

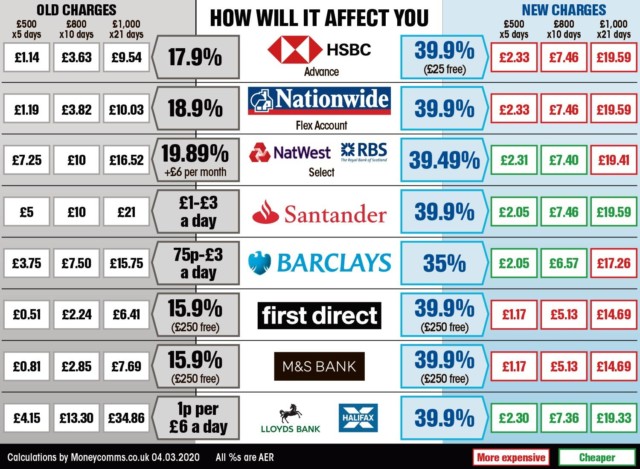

HOW BAD IS IT?

For some, the changes have meant big fee rises, but others have seen a reduction due to flat charges being removed. For example, TSB charges 39.9 per cent but previously it charged 19.84 per cent plus a £6 monthly fee.

If you borrowed £250 for 21 days, you would pay £4.89 now, compared to £8.24.

But HSBC Advance customers, whose overdraft rates have increased from 17.9 per cent to 39.9 per cent, have not benefited.

For the same borrowing, they pay £4.89, instead of £2.38.

WHAT DO I DO?

Whether or not the changes are beneficial to you personally, ask for help with your overdraft if you are struggling due to the impact of coronavirus.

If you have seen your income or expenses hit, ask for the first £500 of the overdraft to be interest-free and for a lower interest rate for three months.

All banks are managing the changes differently, so ring them up to check what help is available.

HOW DO I GET OUT OF THE RED?

Examine your balance, overdraft limit and bank statements to understand how much money is owed. Draw up a budget to see where savings can be made.

As well as cutting back spending, transfer the debt elsewhere to prevent paying any interest.

Nationwide’s FlexDirect account offers a year’s zero- per-cent overdraft, but there is no guarantee on how much of your debt it will cover.

If you do not plan to pay off your overdraft within a year and have less than £1,000, consider switching to the M&S current account. It offers a £250 interest-free overdraft.

If your overdraft is large — more than £1,500 or so — and you are struggling to repay, you could take advantage of credit card firms offering introductory zero- per-cent interest offers.

You will need to pay a one-off transfer fee of about three to four per cent of the debt but then there is no interest for the time of the offer, which is typically up to 18 months.

These are being offered by MBNA, Tesco Bank and Virgin Money.

Keep track of the best fitness smartwatches

WE’VE all been staying indoors a lot more, so maybe this is the time to think about getting fit again.

A smartwatch can help, but which is best?

Sure, you want something that looks good and tells the time very accurately, but what else?

Fitness is a key metric for most smartwatches but some also have GPS built in to accurately measure your outdoor run without your companion phone nearby.

Here are the latest watches I’ve tested, with a range of prices to suit all pockets.

Apple Watch Series 5

BEST ALL-ROUNDER

From £399, Apple

THIS has loads of apps and connects to the mobile network so you don’t need your phone to make calls.

It can take an ECG, measure your heartbeat and warn you if it is too high. If you fall hard and don’t get up, the Watch can call your family or emergency services.

And with four different metal finishes, it looks beautiful.

The latest version has an always-on display so the time is constantly shown, but the earlier Series 3 is still a bargain, priced from £199.

Samsung Galaxy Watch 3

BEST FOR INTERFACE

From £399, Currys

UNLIKE other smartwatches, this has a great feature from regular timepieces – a rotating bezel. Here, it scrolls you through apps and features.

There are plenty of health extras, including heart-rate monitoring.

This is a big, chunky circular watch that’s well built and easy to use. It is probably the best smartwatch for Android phone users.

You are safe to swim with it on and, like the Apple Watch, there’s an option to have a 4G sim built in.

Choose from 41mm and 45mm case sizes.

Huawei GT 2e

BEST FOR VALUE

£139.99, Argos

THE GT 2e has an unusal extra – it is able to measure your blood-oxygen saturation, which can indicate how well your lungs are working.

It also monitors your heart rate continually and, like Apple’s Watch, can warn you if it spots something out of the ordinary.

The device can track different sports and activities including, get this, hula- hooping.

It stands out for a very keen price – and the battery lasts up to two weeks.

FitBit Charge 4

BEST FOR FITNESS FEATURES

£129.99, Argos

FITBIT’s trackers are now so advanced they replace the need for a full-on smartwatch. It has GPS and heart-rate monitoring to make its tracking more accurate.

Its sleep-tracking is excellent, detailed and helpful – though from the autumn the Apple Watch Series 3 and onwards will have sleep monitoring, too.

It can measure your blood oxygen but as part of the sleep measurements.

Battery life lasts up to seven days.

GOT a story? RING HOAR on 0207 782 4104 or WHATSAPP on 07423720250 or EMAIL [email protected]

{kind=link}